All Categories

Featured

Table of Contents

The inquirer stands for a customer that was a complainant in an accident issue that the inquirer chosen behalf of this plaintiff. The defendants insurance provider accepted pay the complainant $500,000 in an organized settlement that requires it to purchase an annuity on which the plaintiff will certainly be detailed as the payee.

The life insurance firm issuing the annuity is a qualified life insurance coverage firm in New York State. N.Y. Ins. are all annuities tax deferred. Law 7702 (McKinney 2002) states in the pertinent component that" [t] he purpose of this article is to offer funds to secure local. beneficiaries, annuitants, payees and assignees of.

N.Y. Ins.

N.Y. Ins. The Division has actually reasoned that an annuitant is the possessor of the basic right granted under an annuity contract and mentioned that ". NY General Counsel Opinion 5-1-96; NY General Advice Viewpoint 6-2-95.

Annuity Rules

Although the owner of the annuity is a Massachusetts corporation, the designated beneficiary and payee is a local of New york city State. Considering that the above specified purpose of Post 77, which is to be liberally taken, is to shield payees of annuity contracts, the payee would be shielded by The Life insurance policy Business Warranty Company of New York.

* An immediate annuity will certainly not have an accumulation stage. Variable annuities issued by Safety Life Insurance Coverage Company (PLICO) Nashville, TN, in all states other than New York and in New York by Protective Life & Annuity Insurance Coverage Firm (PLAIC), Birmingham, AL.

Fidelity Investments Guaranteed Income Estimator

Capitalists should very carefully take into consideration the financial investment goals, dangers, fees and expenses of a variable annuity and the underlying financial investment options before spending. An indexed annuity is not an investment in an index, is not a security or stock market financial investment and does not take part in any type of supply or equity financial investments.

The term can be 3 years, 5 years, 10 years or any type of number of years in between. A MYGA works by tying up a swelling amount of cash to allow it to build up interest.

Kinds Of Annuity

If you pick to renew the agreement, the passion price may differ from the one you had actually originally concurred to. Another choice is to move the funds right into a various kind of annuity. You can do so without dealing with a tax penalty by making use of a 1035 exchange. Since rate of interest are established by insurance provider that offer annuities, it's vital to do your study before authorizing a contract.

They can defer their tax obligations while still employed and not seeking added taxed earnings. Given the present high rate of interest, MYGA has ended up being a substantial part of retired life financial planning - what is a monthly annuity. With the possibility of passion price decreases, the fixed-rate nature of MYGA for a set number of years is very interesting my customers

MYGA rates are usually greater than CD rates, and they are tax obligation deferred which even more boosts their return. A contract with even more limiting withdrawal provisions may have greater rates.

In my opinion, Claims Paying Ability of the carrier is where you base it. You can look at the state warranty fund if you want to, but bear in mind, the annuity mafia is viewing.

They understand that when they put their money in an annuity of any type of type, the company is going to back up the claim, and the market is looking after that also. Are annuities guaranteed? Yeah, they are. In my opinion, they're risk-free, and you ought to enter into them checking out each provider with confidence.

If I put a recommendation before you, I'm likewise placing my license on the line also - can you cash out an annuity. Keep in mind that. I'm very certain when I placed something in front of you when we speak on the phone. That doesn't mean you need to take it. You may state, "Yes, Stan, you said to acquire this A-rated company, yet I really feel better with A dual plus." Penalty.

Best Life Annuity Rates

We have the Claims Paying Capacity of the service provider, the state warranty fund, and my good friends, that are unidentified, that are circling around with the annuity mafia. That's an accurate answer of somebody who's been doing it for a really, extremely lengthy time, and that is that a person? Stan The Annuity Male.

Individuals generally acquire annuities to have a retirement income or to develop cost savings for an additional function. You can purchase an annuity from a qualified life insurance representative, insurer, monetary planner, or broker. You must speak to a monetary advisor regarding your demands and objectives before you get an annuity.

Spia Calculator

The difference between the two is when annuity repayments start. permit you to conserve money for retirement or various other reasons. You do not need to pay taxes on your incomes, or payments if your annuity is a specific retired life account (IRA), up until you take out the earnings. permit you to create an earnings stream.

Deferred and immediate annuities provide a number of choices you can pick from. The options provide different levels of potential threat and return: are ensured to make a minimum passion rate.

Variable annuities are higher danger since there's a chance you can lose some or all of your cash. Set annuities aren't as high-risk as variable annuities since the investment risk is with the insurance coverage company, not you.

Highest Yielding Annuities

If performance is low, the insurer bears the loss. Fixed annuities guarantee a minimal rates of interest, usually between 1% and 3%. The firm could pay a greater rate of interest than the assured rates of interest. The insurer determines the rate of interest prices, which can alter monthly, quarterly, semiannually, or every year.

Index-linked annuities show gains or losses based on returns in indexes. Index-linked annuities are extra complex than dealt with deferred annuities.

Each counts on the index term, which is when the firm computes the passion and credit histories it to your annuity. The identifies how much of the boost in the index will certainly be utilized to compute the index-linked interest. Various other crucial attributes of indexed annuities consist of: Some annuities cover the index-linked interest price.

The flooring is the minimum index-linked rate of interest price you will gain. Not all annuities have a flooring. All repaired annuities have a minimum guaranteed value. Some business make use of the standard of an index's value instead than the worth of the index on a defined date. The index averaging may happen any kind of time during the term of the annuity.

Various other annuities pay substance rate of interest during a term. Compound passion is interest earned on the money you saved and the passion you make.

Annuities Compare

If you take out all your cash before the end of the term, some annuities will not credit the index-linked passion. Some annuities may attribute just part of the rate of interest.

This is due to the fact that you birth the financial investment danger rather than the insurance provider. Your representative or financial consultant can aid you decide whether a variable annuity is best for you. The Stocks and Exchange Compensation identifies variable annuities as protections due to the fact that the efficiency is originated from stocks, bonds, and other financial investments.

What Does It Mean To Annuitize An Annuity

Discover more: Retirement in advance? Consider your insurance coverage. (annuities that pay monthly) An annuity contract has 2 stages: a build-up stage and a payment phase. Your annuity gains passion during the build-up stage. You have several choices on just how you contribute to an annuity, relying on the annuity you purchase: enable you to select the moment and quantity of the settlement.

The Internal Revenue Solution (INTERNAL REVENUE SERVICE) regulates the taxes of annuities. If you withdraw your earnings prior to age 59, you will most likely have to pay a 10% early withdrawal fine in enhancement to the taxes you owe on the interest gained.

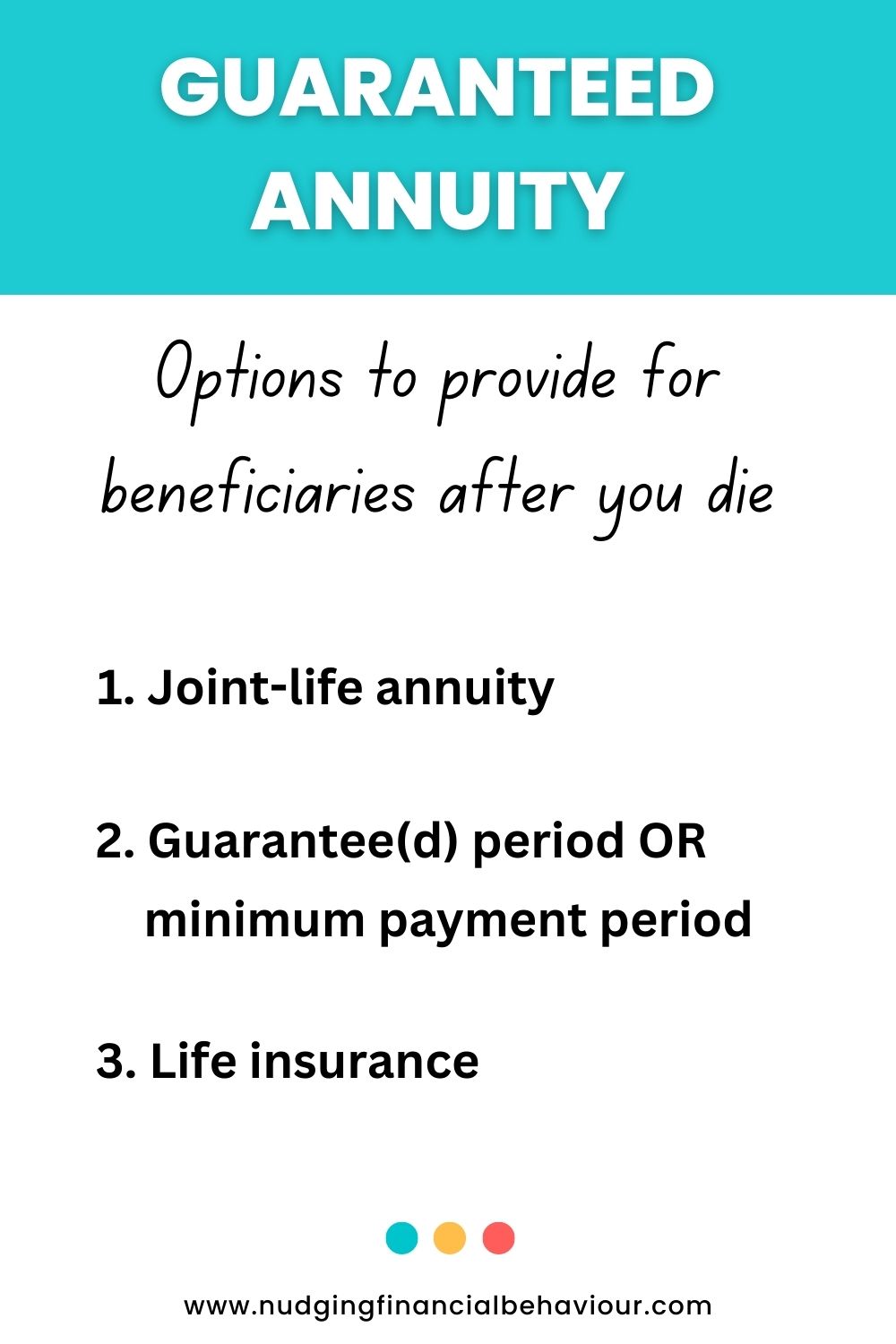

After the buildup phase ends, an annuity enters its payment stage. There are several alternatives for getting repayments from your annuity: Your firm pays you a taken care of quantity for the time specified in the agreement.

Several annuities bill a penalty if you take out money prior to the payout phase. This penalty, called a surrender fee, is commonly highest possible in the early years of the annuity. The cost is typically a percentage of the withdrawn cash, and normally starts at around 10% and drops every year until the abandonment duration is over.

{kind=link}

Table of Contents

Latest Posts

Decoding Annuity Fixed Vs Variable A Comprehensive Guide to Retirement Income Fixed Vs Variable Annuity Defining the Right Financial Strategy Advantages and Disadvantages of Different Retirement Plans

Analyzing Retirement Income Fixed Vs Variable Annuity A Closer Look at Fixed Annuity Or Variable Annuity What Is the Best Retirement Option? Features of Smart Investment Choices Why Retirement Income

Understanding Financial Strategies A Closer Look at How Retirement Planning Works Defining the Right Financial Strategy Advantages and Disadvantages of Different Retirement Plans Why Choosing the Righ

More

Latest Posts